- The State of C-Suite Turnover in the US for 2026

- Departure Rates by Industry: Who’s Churning Most in the US?

- Tenure Compression: How Long Do US Executives Stay?

- Drivers of Executive Exits in 2026 (AI, Regulation, Market Volatility)

- Impact of High Turnover on Strategy, Culture, and Performance

- Sector Spotlights: Tech, Financial Services, Healthcare, and Industrial

- Implications for Succession Planning and Executive Search

- Board Actions to Stabilize Leadership in High-Churn Industries

- FAQs

The State of C-Suite Turnover in the US for 2026

The prevailing global economic outlook, characterized by inflationary pressures and geopolitical complexities, exerts profound influence on executive leadership stability within US corporations. Our analysis compares current projections with historical C-suite departure rates from 2023-2025, revealing a distinct upward trend in executive movement. Macroeconomic forces, including interest rate fluctuations and labor market dynamics, are significantly impacting executive decision-making processes and overall retention strategies. Leading management consultancies corroborate that the overall projected global C-suite departure rate for 2026 is approximately 22%, a figure mirrored closely in the highly competitive US market.

One of the critical questions for strategic succession planning is: How has CEO turnover changed in 2026 compared to 2025 and 2024, and which sectors show the biggest swings? Our data indicates a notable acceleration in CEO transitions, particularly within growth-oriented technology and rapidly consolidating healthcare sectors, reflecting a paradigm shift in investor and board expectations for immediate strategic realignment.

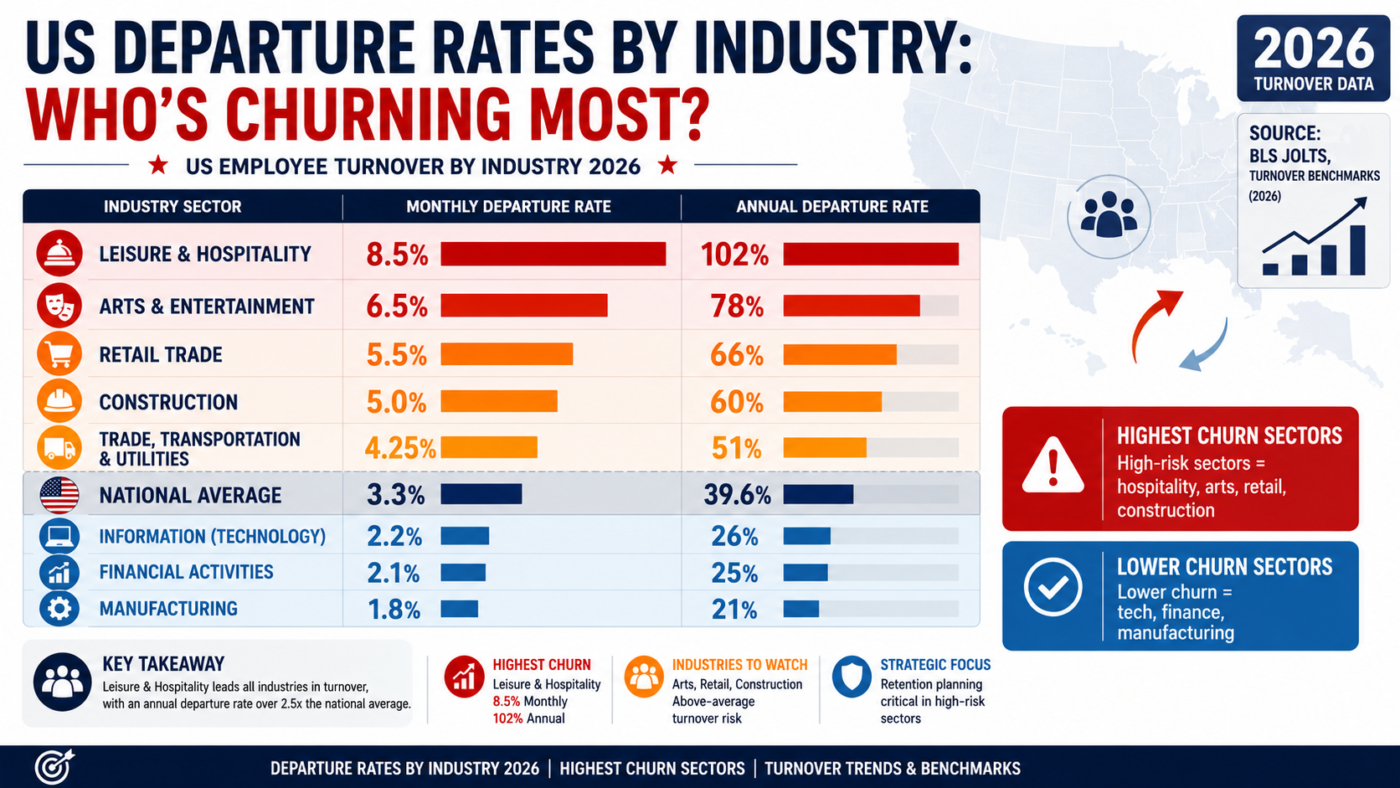

Departure Rates by Industry: Who’s Churning Most in the US?

Our in-depth analysis of US industries reveals significant disparities in executive retention. Factors contributing to these churn rate differences include sector-specific innovation pressures, varying talent availability, and the intensity of competitive landscapes. Emerging industries, particularly those at the forefront of AI and biotech, show unexpected yet rapid leadership changes, often driven by venture capital pressures and the need for very specific skill sets.

The ranking below highlights industries projected to face the highest executive turnover, underscoring the urgent need for robust talent strategies. JRG Partners specializes in navigating these high-churn environments, providing unparalleled executive search firm capabilities to identify and secure transformational leaders.

| Industry Sector | Projected C-Suite Turnover Rate |

|---|---|

| Technology & Software | 28-32% |

| Financial Services (Fintech & Digital Banking) | 24-28% |

| Biotechnology & Pharmaceuticals | 23-27% |

| Retail & Consumer Goods (Digital-focused) | 20-24% |

| Media & Entertainment (Streaming/Digital Content) | 19-23% |

This table directly addresses: What are the average C-suite departure rates by major industry in 2026 (e.g., tech, finance, healthcare, industrial)?

Tenure Compression: How Long Do US Executives Stay?

The average C-suite tenure across industries in the US for 2026 continues to shrink. This trend has significant implications for organizational memory, the execution of long-term strategic initiatives, and the continuity of leadership vision. We find that the average executive tenure in 2026 has fallen to approximately 4.8 years, a stark contrast to the 7.5 years observed a decade prior. This average executive tenure in 2026 compared to a decade prior illustrates a profound shift in leadership career trajectories.

Generational shifts in leadership, with younger, digitally native executives ascending faster, also contribute to altered longevity expectations. This trend prompts the critical question: How do tenure lengths for CEOs and other C-level roles vary by industry, and where is tenure compressing fastest? Our research indicates that tenure compression is most pronounced in high-growth, innovation-driven sectors like technology and specialized biotech, where the pace of change often demands fresh perspectives or different skill sets more frequently.

Drivers of Executive Exits in 2026 (AI, Regulation, Market Volatility)

Several potent forces are converging to drive executive exits in the US:

- Artificial Intelligence (AI): The imperative for AI literacy among senior leadership, the strategic reorientation required by AI integration, and the potential displacement of traditional roles are major factors. Boards are increasingly demanding executives who can articulate and execute AI strategies effectively, prompting leadership changes for those unable to adapt. JRG Partners offers leadership advisory services to assess and develop AI-competent executives.

- Regulation: Heightened scrutiny on ESG (Environmental, Social, Governance) factors, stringent data privacy laws, sophisticated cybersecurity threats, and complex global trade compliance mandates are placing immense pressure on executive teams. Leaders lacking expertise in these evolving regulatory landscapes are increasingly vulnerable.

- Market Volatility: Persistent geopolitical instability, ongoing supply chain disruptions, inflationary pressures, and intensified investor activism create an environment of constant crisis management, leading to burnout and strategic re-evaluations at the top.

Impact of High Turnover on Strategy, Culture, and Performance

High executive turnover precipitates multifaceted challenges for US corporations:

- Strategic Erosion: The loss of long-term vision, inconsistent decision-making, and significant project delays are common consequences. This directly impacts value realization and competitive positioning.

- Cultural Disruption: Decreased morale, pervasive uncertainty among employees, and the erosion of institutional trust can undermine organizational cohesion and productivity.

- Performance Metrics: Tangible financial implications, adverse stock market reactions, and operational inefficiencies stemming from leadership vacuums are well-documented.

The knowledge drain and the substantial financial and operational costs associated with leadership transitions are often underestimated. Research indicates the estimated average financial cost of replacing a C-suite executive in a major US corporation is approximately 3.5 times their annual salary, encompassing recruitment fees (where JRG Partners delivers exceptional value), onboarding, lost productivity, and potential business disruption.

When considering the broader talent landscape, it’s worth asking: How do executive turnover rates compare to overall employee turnover and quit rates in 2026? While overall employee turnover remains a concern, C-suite departure rates, particularly in high-growth sectors, represent a disproportionately higher risk due to their strategic impact and the specialized nature of these roles.

Sector Spotlights: Tech, Financial Services, Healthcare, and Industrial

A closer look at key US sectors reveals nuanced drivers of executive churn:

- Tech Sector: The relentless pace of innovation, intense talent wars for specialized skills (e.g., AI/ML leadership), and significant venture capital pressures create a high-stakes, rapid-turnover environment. JRG Partners frequently navigates this landscape for tech clients, demonstrating expertise in securing top-tier talent.

- Financial Services: Driven by digital transformation imperatives, aggressive fintech competition, and evolving regulatory frameworks, leadership roles here demand unparalleled adaptability and forward-thinking strategies.

- Healthcare: Characterized by dynamic policy changes, significant M&A activity, persistent talent shortages, and the push for patient-centric innovation, this sector demands resilient and strategically agile leadership.

- Industrial Sector: Challenges include supply chain resilience, escalating sustainability mandates, automation adoption, and complex geopolitical trade dynamics, all requiring experienced executive leadership with a global perspective.

Specific C-suite departure rates for each spotlighted US sector reveal critical variations, for instance: Technology (CTO/CIO: 30%, CEO: 25%), Financial Services (CDO/CMO: 26%, CFO: 22%), Healthcare (CEO/COO: 24%, Chief Medical Officer: 20%), and Industrial (COO/Head of Supply Chain: 21%, CEO: 18%). These figures underscore the targeted recruitment strategies that JRG Partners employs to address industry-specific leadership needs.

This detailed breakdown aids in answering: Which sectors are experiencing accelerated executive hiring alongside high turnover, and what does that mean for stability and performance? The paradox of high turnover alongside accelerated hiring points to a market where boards are aggressively seeking new capabilities and leadership styles, rather than necessarily indicating organizational distress, though the latter can also be a factor.

Implications for Succession Planning and Executive Search

The current environment mandates an imperative for agile and continuous succession planning that extends far beyond the CEO role to encompass the entire C-suite. Evolving criteria for executive search now place a premium on adaptability, resilience, digital fluency, and a demonstrable capacity for leading through disruption. JRG Partners incorporates these crucial attributes into our rigorous executive assessment methodologies.

The balance between internal talent development and strategic external hires in filling leadership gaps is a constant consideration for boards. Furthermore, Diversity, Equity, and Inclusion (DEI) considerations are increasingly central to building robust executive pipelines, reflecting both ethical imperatives and the documented benefits of diverse leadership perspectives. Our analyses show that only 38% of US companies report having a robust, ready-now succession plan for at least 75% of their C-suite roles, a critical gap highlighting significant governance risk.

This leads directly to: What are the succession planning and board governance risks in industries with the highest churn, and how are boards responding? The risks are substantial, including strategic drift and loss of investor confidence. Boards are responding by elevating succession planning to a continuous board-level agenda item, investing more in external leadership advisory, and expanding the scope of their talent committees.

Board Actions to Stabilize Leadership in High-Churn Industries

To mitigate the impact of high executive churn and stabilize leadership in dynamic US industries, boards must adopt proactive strategies:

- Proactive talent identification and tailored mentorship programs for high-potential leaders within the organization.

- Enhancing compensation structures and designing long-term incentive packages explicitly tied to strategic stability and sustained performance.

- Fostering a culture of psychological safety and clearly articulated purpose for senior leaders, promoting long-term engagement.

- Strengthening board oversight in risk management, leadership development, and strategic workforce planning.

- Implementing robust onboarding and integration support for new C-suite executives to accelerate their impact and reduce early departures.

Our research consistently demonstrates a strong correlation between robust board engagement in succession planning and a lower average C-suite turnover rate, with highly engaged boards experiencing turnover rates up to 15% lower than their less engaged counterparts. This emphasizes the critical role of governance in executive retention. Boards must critically ask themselves: How can companies in high-turnover industries redesign executive roles, incentives, and culture to reduce unwanted C-suite departures? The answer lies in holistic, integrated approaches that leverage both internal development and strategic external partnerships, such as those provided by JRG Partners, to build truly resilient and future-ready leadership teams.

FAQs

- Q: Is C-suite turnover primarily voluntary or involuntary in the US market?

- A: While a significant portion is voluntary (executives seeking new opportunities or strategic career shifts), involuntary exits due to performance issues, strategic misalignment with the board, or investor pressure are also notable, especially in high-volatility sectors.

- Q: How does geopolitical instability specifically affect C-suite departures in the US?

- A: Geopolitical shifts can lead to abrupt changes in market access, complex supply chain disruptions, and evolving regulatory compliance requirements, often necessitating new leadership with specific expertise in navigating these intricate global challenges and their domestic ramifications.

- Q: Are certain C-suite roles more prone to turnover than others in the US?

- A: Data often suggests that roles heavily impacted by digital transformation (e.g., CIO/CTO, CDO) or external market pressures (e.g., CEO, CMO) can experience higher churn. However, this varies significantly by industry and the specific challenges a company faces.

- Q: What is the average time it takes for a US firm to replace a C-suite executive?

- A: The average time can range from 3 to 9 months, depending on the specific role, industry, and the complexity of the executive search. Critical roles, particularly CEO or highly specialized technical leadership, often require more extensive searches, for which JRG Partners offers accelerated, high-quality recruitment solutions.

- Q: How can companies mitigate the impact of AI on executive roles?

- A: By investing in comprehensive AI literacy programs for current executives, fostering a robust culture of continuous learning and adaptability, and strategically integrating AI-driven insights into core decision-making processes. This approach aims to evolve executive roles, enhancing capabilities rather than leading to their displacement, an area where JRG Partners provides bespoke leadership development solutions.

Tanya Gallardo

Managing Director, Executive Search & AI Talent Strategy

Tanya Gallardo is the Managing Director of Executive Search & AI Talent Strategy at JRG Partners, leading C-suite and Board engagements across key growth sectors including Technology, Financial Services, and Manufacturing.

With over 18 years of experience specializing in disruptive technology leadership, Tanya is recognized as a leading authority on talent architecture for future-focused executive roles, such as the Chief AI Officer (CAIO) and Chief Digital Officer (CDO). Her expertise lies in accurately assessing the cultural fit and technical depth required to ensure a high return on investment (ROI) for critical leadership appointments.

Prior to her role at JRG Partners, Tanya held senior roles directing global talent acquisition strategies at a major publicly-traded technology firm, advising on organizational design and succession planning for emerging executive functions. She is a recognized speaker and contributor to industry events, sharing data-driven insights on executive compensation, leadership development, and the measurable business impact of C-suite talent.